This interview appeared in the ET Prime on 5th January, 2023 (link)

India is the global back-office and world’s pharmacy, says Ravi Dharamshi, founder and CIO, ValueQuest, speaking about IT and pharma sectors – the two top themes of the last two decades.

In conversation with Ami Shah, he talks about the SCALE framework of investing, stock-market lessons learnt from Warren Buffett and late Rakesh Jhunjhunwala, and things that motivate him.

Are you a value or a growth investor? Why do you say that? We honestly do not wish to get stuck or typecast in the nomenclatures of growth or value. ValueQuest means itself the quest for value. Growth is inherent and an integral part of value realisation. Lot of value stems from the future growth. Our approach has been to find companies that are on the cusp of a growth phase and identify them before the market has baked the future expectations into the price.

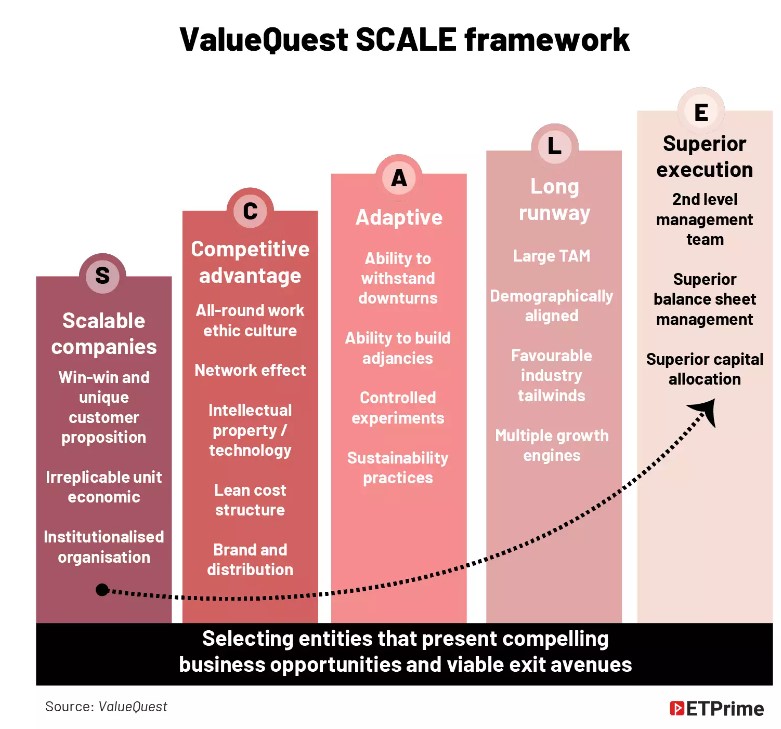

Our goal is to identify ideas or themes that will do well in the foreseeable future of 3-5 years. Connecting the dots top-down, we set out to look for best companies which can capture the opportunity in this theme, and in the process change the SCALE of the company itself.

SCALE framework: Scalable companies with sustainable Competitive advantage, Adaptive on a Long runway with superior Execution capabilities. We believe this is the phase wherein maximum wealth creation happens for a company and that is what we aspire to capture.

What are your learnings from a value investor like Warren Buffett? He also bought Apple at its peak and today it accounts for 40% of his portfolio. Warren Buffett is the fountainhead of investment learning and lessons and there is so much one can learn and imbibe. For a fund manager or even a normal investor to imbibe his thought process to whatever extent possible should be the first step in the journey of wealth creation.

His quotes and sayings are investment folklore and there are no qualms for us to say that we use his quotes wherever and whenever possible. There is so much wisdom packed into few words.

But from the above example or question, I think the biggest learning is that he is not afraid to change his mind and views and admit his mistakes. From not being too keen on technology companies for various reasons and not having any in his portfolio to having his largest holding in Apple, which has rewarded him well. His flip flops on the airline industry are also well known and his letters to shareholders are full of self-deprecating humour, which is refreshing and brings out a character of humility that is so critical in the investment world.

What according to you were the top 3-5 themes for the last decade? Two top themes in the last two decades have been IT and pharma. Both industries have gone through the cycle of discovery where cost efficiencies and technical edges were explored and exploited to the cycle of growth. They went through periods of consolidation and eventually innovation and only the best survived. Finally, they are closer to the mature stage in terms of growth and return on capital.

These industries have proved themselves to the world and put India on the map with their scale and ability to seize the opportunity as and when they were presented, be it Y2K or Covid-19. These have also been rewarding investors, with IT giving a 17% CAGR over the past two decades. India has gone on to become the global back-office and the world’s pharmacy.

How important is ESG in your investment philosophy? What are the parameters you look at? Mark Twain, famously mentioned in his autobiography, “There is no such thing as a new idea. It is impossible. We simply take a lot of old ideas and put them into a sort of mental kaleidoscope. We give them a turn and they make new and curious combinations. We keep on turning and making new combinations indefinitely; but they are the same old pieces of coloured glass that have been in use through all the ages.”

ESG or Environmental, Social and Governance is one such old cocktail. It’s the latest buzzword in the investing world, even if it’s not really new, is one such old idea that is being put through a different lens, every few years.

It will be safe to assume that companies and decision makers, who have a fiduciary responsibility to maximise profit or shareholder value, are incentivised for better performance. However, its very tough to assume they to work solely with the higher goals of ESG in mind and not worry about shareholder satisfaction.

On the other side, societal expectations and requirements for a sustainable future are absolutely essential and need a lot of focused attention and questions asked. However, the definition of sustainability and its framework may differ from country to country and company to company. Further, ESG non-compliance will probably be a key factor going ahead in raising funds/investments and tapping other markets or avenues.

As an investor, having a feel-good factor that you are participating in the change, which is good for the future, may not be the most best investment for returns per se and one may have to walk a thin line between the high road and high returns.

So, it’s our endeavour to find such companies and themes that will benefit in the move towards ESG compliance — be it a transition to renewable energies and ancillary businesses around this.

Which are the new themes that you are exploring seriously? We have entered exciting times post-Covid-19. As I have mentioned in of our earlier posts, “This is the manufacturing renaissance for India”. There is a shift in the world order and there is a need across the globe to look for alternate suppliers or manufacturers to the products needed by the world. Days of China being the lowest cost and most reliable supplier to the world are incrementally over. Also, the world has realised how much it depends on China. So, the need to reduce dependence is clear and present. Be it in industries as diverse as chemicals or smartphones, the theme of China + 1 will not be a temporary one, but a paradigm shift is on the way. For example, India has replaced Vietnam as the world’s second-largest mobile phone manufacturer. Between 2016 and 2022, India is expected to attract investments worth INR44,265 crore in the smartphone manufacturing sector.

From just three mobile manufacturing units in 2014, India witnessed a jump to 268 smartphone and allied services manufacturing units until 2018.

This has also been massively aided by schemes and intent of the government in its endeavour for Atmanirbharta, be it in defence, textiles, electronics or capital goods. Schemes like PLI have further bolstered Indian companies to relook and enhance manufacturing and reclaim the market share lost to China and Vietnam.

Another theme, which has been very interesting in the last few years but has really come to the fore since the Russia-Ukraine war is the transition away from fossil fuels. Energy literally came under fire and while the push for reduction of dependence of imported fuel has been a long-standing push, the impetus towards renewables, be it solar, wind or even hydrogen, has been extremely high. This and its ancillary businesses could be a great idea for the future.

How do you look at high PE stocks in terms of quality stocks? When should investors completely ignore high PE stocks? My first boss and my mentor, Late Rakesh Jhunjhunwala, always used to say it’s more important to buy at the right price. He often used to say, “Never invest at unreasonable valuations. Never run for companies which are in limelight.” He strictly followed this rule and used to advise New Age investors to look at stock valuations before making any investment decision. This holds true even in today’s world of high-priced IPOs and we have seen how that has played out for some of them. While they may be good businesses, it’s not necessary that good businesses bought at any prices or unreasonable valuations will be rewarding for investors. Having said that, there is a certain higher PE command for high quality stocks, these 50x, 55x, 60x multiples can be a bit misleading. They also need to factor in the future growth possibilities for an investor.

Markets give higher multiple to businesses with:

Higher predictability

Higher profitability

Higher growth and longer runway

Higher sustainability of profits due to competitive advantages

So, as Warren Buffett changed his approach from an absolute cigar butt-oriented value investing to Phil Fisher approach of buying superior companies.

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” – Warren Buffett

We also believe in buying superior quality companies, but even that has an entry multiple to it. Valuations do form a major portion of future returns.

One must ensure not to end up giving a high multiple to a business which is sub-scale, sub-quality and where profits are not sustainable due to cyclicality or other reasons.

Given a chance would you prefer to be a highly concentrated investor? Higher concentrated bets and a low churn rate are our most favoured and ideal scenario. Here also I would like to quote the Oracle of Omaha, “Diversification may preserve wealth, but concentration builds wealth.”

The level of concentration is a matter of personal choice and ability to withstand market vagaries. It is a question of your ability to hold positions for long periods of time. If an external event can force your hand at the wrong time, then you are better of more diversified. We believe 8-12 stocks is ideal concentration for a portfolio.

Do you believe in timing the market? If yes, how do you do it? “Time in the market is more important than timing the market.” However, when Buffett urges you to buy, when everyone is fearful and sell when everyone is greedy, is also essentially a way to time the market. We wish to be long-term greedy. Our time horizon is 3-5 years. We usually have one 30% correction, two 20% correction and three-five 10% corrections in a 5-year horizon. Our aim is not to get every correction right. But when opportunity presents itself, it is our duty to take that advantage.

We try to be on the right side of the trend and within that we stay invested if the stock and business fit in our hypothesis and valuation matrix. We don’t try and get the bottoms and we certainly don’t try and judge the tops. We hope we can buy reasonably good businesses in an emerging theme, and we hope the business can grow to its potential. We cannot have an investing strategy that focuses on the extremes of the market all the time. In fact, focusing on the same can be very counter-productive. Every future market correction seems like a threat and every past market correction was an opportunity in hindsight. If we give up our obsession with finding the extremes in the market, it will take away most of our worries.

How seriously you look at macro-economic issues. How do you factor it into the investment philosophy? There is no doubt that macroeconomics plays a very important part in the evaluation of a business, and also how they will impact the market scenario. In fact, the recent memo of Howard Marks is an excellent representation of this — how the macro-economic factors, say interest rates, have impacted and affected asset classes and eventually market performances over the past 2-4 decades. Having said that, investing is part science and part art, and we have seen countless examples of this. In a favourable environment in 2017-18, while the world outperformed, India was dealing with more structural changes that gave us short-term pains. But on the long run, there’s a promise to become invaluable and eventually, as we call it at ValueQuest, it will make India ‘anti-fragile’ to some of the global macroeconomic headwinds.

Further it’s our goal to not look at day-to-day weather patterns but seasonal changes. This broad understanding of the season we are in, whether it’s time to be more aggressive or defensive. Our macroeconomic study is to ensure that we are factoring in the right models and frameworks given the seasons versus the variables of day-to-day weather vagaries.

What are your parameters for investing into deep-value stocks? How do you analyse the promoter? Since we do not label stocks into growth or value paradigm, our parameters for investing do not change. Broadly, business, promoter/management and valuations remain the criteria for investing. However, in case of smaller companies, promoter/management have far higher weightage in terms of significance.

Our framework for analysing any company management broadly follows:

Integrity – Judged through past actions

Competency – Judged through ability to manage balance sheet during downturn, ability to gain market share, expand addressable opportunities

Alignment of interest – Judged through skin in the game, corporate structure and past actions related to minority shareholders

Allocation of capital – Ability to generate returns above cost of capital over a long term is the true test of any management.

What was the best book or article you read last year? Why did you like it? It’s actually a re-read of a book. Reminiscences of a Stock Operator: The Life and Times of Jesse Livermore. This book is a wonderful read. No matter how many times you have read it, the book leaves with you some new lessons. Not so surprisingly, it has quotes and enough anecdotes that still resonate almost 100 years after it was first published.

This is the beauty of that book, and this is the beauty of the stock market. It generally repeats and rhymes. For example, one quote in the book reads, “Carefully laid plans will miscarry because the unexpected and even the expectable will happen.” And see how true this has been in the year gone by. Twelve months ago, we were on the way of a commodity supercycle, today we are struggling with a possibility of recession. A year back, we were on the steroids of “free, easy, fast” money, today we are looking at rising interest rates, QT and a much-needed funding winter. Today, its king dollar / rising yields and tomorrow it may be something else.

“The real key to making money in stocks is to not get scared out of them.” – Peter Lynch

Which sports you enjoy? Which match or event was memorable last year? Year 2022 has been great for sports. I was lucky enough to catch the live India-Pakistan cricket match in Australia, and also witnessed one of the greatest football world cup finals in the history just recently. Both were absolutely enjoyable watch, and both were taken to the ultimate last minute to decide the winner. I have seen and played a lot of sports, but these both games were something else. The winner is sports and while there are so many lessons being eulogised, you cannot but not mention the never-say-die spirit of the runner ups in France and laud the genius and longevity of the career Lionel Messi has had. Hats off.

Which was your inspirational song last year? So many. I am a complete music buff, and the taste varies from Kishore Kumar to Imagine Dragons. So, there is not a single song that I can pinpoint. However, Don’t Stop Believin’ by Journey is one of the better inspirational songs I have heard. As the lyrics go – Don’t stop Belivin, Hold on streetlights, People.

Name some movies or TV serials you have enjoyed over the last one year. This year has been for sports documentaries and there have been so many good ones. Two that stand out are Swimmers and Rise, both are about migrants making it against all odds and succeeding under the most adverse circumstances.

Rise, particularly, has had a real fairytale ending with Giannis Antetokounmpo ending up as NBA world champion in 2021 and getting two-time MVP awards. His story, grit and determination has been certainly special.

Tell us your favourite stock market anecdote involving a colleague or an acquaintance. There have been so many, but two are most memorable. In 2007, when I was in far more illustrious companies amongst the giants of our stock market, they made a statement that the market is going at 100 KM/hour and an accident is around the corner. This statement had so much wisdom and eventually when the global financial crisis precipitated, it made so much sense for a young inexperienced investor like me. This profound wisdom and the logic behind it will remain an eternal lesson for me.

My own small such experience was in the despair of Covid-19 where I publicly stated, “One should sell their house and buy stocks.” While I only meant it metaphorically and wanted to emphasise the opportunity that lay ahead, I got a bit of flak for it. Even though it eventually worked out superbly well for those who did invest in those times, it also taught me a good lesson on standing out on my own conviction and literally keeping my head when everyone was losing theirs.

I must confess, 2022 ended up being far tougher than I thought it would be.

Coming post a tumultuous couple of years with wild swings amidst once in a lifetime pandemic, a collapse of the world economy, the opening up of the world, we saw it all. From negative crude prices to peak crude. From stimulus driven liquidity to tightening rates and purses. From closed shipping routes & freights to the sky and now submerged. From various coins to the moon and back. From commodities which glistened in the sun to back to earth. These were days where years happened.

But amidst all this turmoil, India was standing out as an oasis of growth, stability, and bullishness. Which it did, well at least at the index level it seems all good. But below the surface markets have been far tougher than imagined. Just proves the point, even if you get your macro reasoning and portfolio positioning correct, it is not possible to have a performing portfolio all the time.

A year where the macros could take maybe a small backseat and the businesses could take ringside seats & truly live up to their potential. An opening up trade, a softening of commodities, green shoots in the economy and the animal (read bullish) spirits should have been raring to go.

Mr. Market also had its way with traders / investors akin, The FII’s pulled out big, India would have normally collapsed, instead it’s been rock solid. ESG was supposed to be the theme of the decade, Non ESG stocks had the time of their life this year. Pharma and IT with its hangover in terms of demand and efficiency in a Covid and post Covid world was supposed to have a long runway and were seen as pockets of value and growth, they are amongst the worst performing sectors this year. Private Banks were eating PSU banks market share for lunch, guess who outperformed this year. PSU bank stocks outperformed by a mile. India used to import almost all its defence requirements, not anymore, defence manufacturers and ancillaries are amongst the best performing stocks this year

Despite all of this, not to a surprise to the believers, Indian equity has managed to outperform most asset classes by a wide margin and while Indices flirt with all-time highs, there are common themes & musings you hear within the investor cycle and their portfolios and the disconnect it has with the index.

Such a year definitely calls for some introspection and especially keeping in mind the spirit of the season, the resolutions, the picks of the year, the lessons and threads it brings to us. These are some of my notes for introspection.

Note to Self – second and third order implications are not apparent easily. And on top of that market reaction to the same is even more difficult to predict.

“If the unusual never happened there would be no difference in people and then there wouldn’t be any fun in life. The game would become merely a matter of addition and subtraction. It would make of us a race of bookkeepers with plodding minds. It’s the guessing that develops a man’s brain power. Just consider what you have to do to guess right.”

This year has been strange but in a manner which has been unique and challenging and has often been at loggerheads with its own self in many ways.

The world opened up and declared the end of a pandemic and China went back to lock down and a Zero Covid policy. Europe has been ravaged by war for a greater part of the year and this has caused not only geopolitical implications and see saws, but it has resulted in great economic imbalances, be it energy crisis or shutting of supply chains.

While this appears to be out rightly bleak news, it has brought up tremendous opportunities for India, be it China + 1 / Europe + 1, Atmanirbhar Bharat, the cause of strengthening our defence capabilities or the Renewable Energy push

Timing anything in the stock market can be quite difficult, and that includes recessions. It’s also quite possible a recession will occur before anyone knows and won’t be declared until it is well underway or over. Stay Invested and Stay focused on quality of your business rather than focus on economic outcomes.

Note to Self – Whatever happens in the stock market to-day has happened before and will happen again.”

Not much long ago, words like Defi, Crypto Punk were the buzz words and the future, not being in them, evinced laughter, and scorn. 2022 pushed Crypto over the cliff, the monkeys vanished, and companies and businesses built on empty promises, unsound practices (Including some of our overvalued & much hyped IPO’s) were punished and some would argue not suitably enough. While there is much value in technologies like Blockchain and some of our “ new age” companies do have the potential to turn the corner and reach scale and size in the next decade, this year has not been pretty & this has happened since time immemorial, be it the Tulip Mania, Dot Com bubble or the inflated real estate stocks, every time there is a new “fad” in town there is someone else holding the bag and its always a lot lighter.It’s never different this time.

Note to Self – Be long-term greedy.

“Speculators buy the trend; investors are in for the long haul; “they are a different breed of cats.” One reason that people lose money today is that they have lost sight of this distinction; they profess to have the long term in mind and yet cannot resist following where the hot money has led.”

Markets at times have a feeling of Neighbours Envy, when everything around you is rising & you question your own hypothesis and principles. When you buy a theme you envisage a certain possibility, but at times get carried on with the daily noise and gyrations and you lose your head, cool and eventually your take your eye of the ball. Classically also known as FOMO, this has continued to ravage investors over the years. When we forget the distinction between buying businesses which will seize the scope of potential ahead versus companies that may tend to rise like how all boats rise with a full tide & only when the tide turns, do we know, who all will float or sink.

To be in for the long haul is where the magic happens.

Note to Self “I do not allow my possessions—or my prepossessions either—to do any thinking for me.”

Biases are part of human emotion, and it generally affects our investment decisions even when they are as system driven as possible. Coal is a dwindling source of energy; PSU stocks are untouchables and State run banks are glaring with inefficiencies are just some of the examples

Leaving our biases, be it hindsight, confirmation, information, or recency aside and thinking with a clear mind has become an important skill in the world of investing.

“What you see is important, what you cannot see is more important.”

Note to Self – Carefully laid plans will miscarry because the unexpected and even the expectable will happen.”

12 months ago we were on the way of a commodity super cycle, today we are struggling with a possibility of recession. 12 months ago we were on the steroids of “free – easy – fast” money, today we are looking at rising interest rates, QT and a funding winter. Today its king dollar / rising yields and tomorrow it may be something else.

“There will always be something new & in this every changing world.“

“The real key to making money in stocks is to not get scared out of them.” – Peter Lynch

History has always rhymed, and the stock market is the best example of this. It’s also the place where generational wealth has been made. The only thing we should be clear is our goals, our objectives, and what businesses we are buying and why.

“Know what you own and why you own it” – Peter Lynch

Have a great new year 2023 & see you all on the other side.

Ravi Dharamshi

CIO

ValueQuest Investment Advisors Pvt. Ltd.

Sometime between the 6th and 8th century, all the Gods and Devas came to Lord Shiva with a strange predicament. Having seen into the future, they realised that Planet Earth is going to be quickly depleted of all its resources and man being man, will soon run amok and destroy the planet. Energy which is known as the fuel of life, will soon be at a severe shortage and the future of wars will be fought over them.

The God’s predicament was that they needed to communicate a message to mankind thousands of years into the future, a message which will not only be communicated, interpreted but also understood well enough to save Earth. Lord Shiva & Goddess Parvati patiently heard this worry and told the Gods to not worry, they have the perfect solution to all of this – Lord Ganesha –

There is an explanation on the internet which says “Ganesha, in fact, is the symbol of he who has discovered the Divinity within himself. Ganesha is the first sound, OM, in which all hymns were born. When Shakti (Energy) and Shiva (Matter) meet, both Sound (Ganesha) and Light (Skanda or Kartikeya) were born. “

Before we go ahead, the above story is purely fictional and a figment of an omnist mind, we have absolutely no way in knowing what transpired so many years ago and nor have we read the holy texts to interpret the same. What is, however, not fiction and is playing out today, wars are being fought over energy and fuel, there is shortage and severe crisis and the climate change has heralded a need to conserve energy and transit to renewable resources to ensure a longer sustenance.

Made from soil, immersed in water, radiant like the sun and son of energy and matter. What if the entire festival of Lord Ganesha is an aphorism for us to become one with nature.

What if this all part of master plan of Lord Shiva to save Planet Earth, having realised that there will be shortage of fuel & energy and the only way we can be saved as time goes by, humans will have to go back to their roots and look for answers there.

The answers maybe are found in the holy festival of Ganesh Utsav. If there would be one festival which truly unites India across the spectrum of religions and classes, it’s probably this one. Time spent in the lines to worship the more popular and revered mandals, will validate this notion as you are generally surrounded by a variety of devotees from different backgrounds all united by a common Shraddha or faith.

The legend of Lord Ganesha has so many environmentally positive stories connected with him, it’s almost profound on the message he tries to convey to us.

From his infamous “eco-friendly – energy saving” trip around the world, to his creation from earth and soil to his immersion in water, to his “re-usability” of the elephant face, his mouse carrier & finally to the growing awareness of eco-friendly adaption to this holy festival, there seems to be a virtuous cycle of awareness and realisation set in place which augurs well for the generations to come.

Several potters, sculptors, artists, and idol makers from across the country have been creating awareness amongst the people about eco-friendly Ganesh idols made by using clay and soil from lakes and rivers in the city. This is truly an effort to conserve the environment and promote traditional customs and art forms. It is very essential to change the mindset of people and make them aware and adopt eco-friendly practices. The demand for eco-friendly Ganesha idols has been on the increase, this definitely is a healthy trend. The call for such awareness has seen many different practices being followed across the country. Just as we have moved to eco-friendly celebration of Ganesha, we need to move to renewable energy sources.

The history of mankind has been a lesson in energy transition, from agrarian fuels, fossil fuels, nuclear energy, energy has come a full circle to going back to agrarian or biomass, solar and hydro fuels which will not only be environment friendly, but also will prevent conflicts.

It is pertinent to however note that environment consciousness is nothing new for India and it is a cause to which India has long been committed. Protection and preservation of the earth, natural resources, and wildlife are enshrined in Indian ethos, culture, and tradition. From the Vedas and the ancient Sanskrit scriptures (1500 to 1000 BCE) to the royal edicts by Emperor Ashoka (268 to 232 BCE), Indian culture has often invoked concepts of harmony between life and nature.

As home to approximately one-sixth of humanity and one of the world’s most youthful nations, India’s role in making the planet better and sustainable is crucial. Now is the right time to act if India wants to protect the planet and ensure a healthy life for the present and future generations.

So, while we celebrate this festival, we take inspiration from the so many hidden lessons which Lord Ganesha conveys, management lessons, investing lessons and so on, maybe there is a renewable lesson for us as well. Direction for us to become one with nature across the board. The lesson is to move to renewable energies and fuels. The lesson is to conserve planet earth for a better tomorrow.

On this occasion, we invoke the verse in Ganesha Mantra and pray for wisdom and the removal of obstacles for all.

Vakratunda Maha-Kaaya Surya-Kotti Samaprabha

Nirvighnam Kuru Me Deva Sarva-Kaaryeshu Sarvadaa ||

Back in 2013, India found itself relegated to the pack of ‘fragile five’ emerging markets. It has been a long and painful journey but India today is well and truly on its way to carving its own niche and becoming Antifragile in this fragile world.

Presentation made by Our CIO, Ravi Dharamshi @ India Investor Conclave (IIC season 8) at Goa in Dec 2021.

Summary of Presentation:

1. There has been tremendous wealth creation in Specialty Chemicals sector – 60x in 7 years.

2. Currently market has priced the sector to perfection and is ignoring all the inherent risks.

3. Long-term opportunity might remain but odds are tremendously out of favour for the sector from next couple of years point of view.

Our CIO Mr. Ravi Dharamshi was recently interviewed by Mr. Vivek Bajaj, co-founder of StockEdge and Elearnmarkets. Our CIO spoke about successful investing, he has elaborated on the VQ Investing Framework. He discusses at length various aspects of the framework and the process VQ follows.

India stands at the cusp of a stronger economic growth for longer. Never have the conditions been so favourable for Indian Economy as well as Indian corporates. This presentation tries to substantiate the same claim.

Pratikraman – “Prati” means “back” and “kraman” means “to go”. It means to go back, to reflect and review, to confess and atone, asking for forgiveness from others for one’s own faults of mind, body, and speech in one’s daily activities, and forgiving faults of others and extending friendship to all.

Paryushan parva is the king of all festivals for whole Jain community. It is a time for self-analysis and soul searching, it provides a break from routine life and allows us to reflect and contemplate on our past conduct. Paryushan is not just a festival to rejoice and celebrate; instead, it is a ‘parva’ in which all Jains try to discipline themselves. People try to live with the utmost simplicity.

It is a time to reflect, introspect and seek forgiveness. Everyone needs a reset button, a Ctrl-Alt-Del mode where we can just reboot and restart. We often, especially in the markets wildly sway between our emotions and most of us wish that we could have just done somethings differently or behaved differently or given another chance, when faced with defining moments.

While it’s impossible to go back in time and rectify your outer deeds, it’s easier to clean, audit and analyse our inner balance sheet, our inner score card & the significance of Paryushan in Jainism is one such opportunity which can be analogised with our journey as investors. Its founding pillars have many valuable lessons to imbibe, and we can draw so many parallels for them in the investing world.

Paryushan stands for practices like Non-Violence (Ahimsa), Self-discipline (Sanyam), Fasting (Tapah), Study of scriptures (Swadhyay), Introspection (Pratikraman), Repentance (Prayaschitta). Incorporating and applying these practices as process in your investing process can tremendously improve one as an investor.

Ahimsa – In Jainism, ahimsa is the standard by which all actions are judged. Practising ahimsa makes oneself aware of their environment. It makes people more empathetic towards others, which makes us humble. Jainism tries to imbibe humility in individuals by making them appreciate the tiniest of living being and empathising with them.

Humility is an important trait for an investor. As they say, there are old investors and there are bold investors, but there are no old and bold investors. It is because market has humbled them many a times and they have learnt their lessons. Humility is a discipline that can help protect investors from letting their emotions overrule their common sense.

Sanyam – Jainism encourages Individuals to maintain whatever self-control is possible.Discipline and self-control are a large factor to navigate the various ups and downs of the market. As Warren Buffet says “We don’t have to be smarter than the rest. We have to be more disciplined than the rest.”

Tapah – Fasting instils discipline and helps in building will power to delay gratification. According to Jain texts, abstaining from the pleasures of the five senses such as sounds and dwelling in the self in deep concentration is fasting (upavāsa). Knowing your circle of competence and ‘practicing’ upvas’ of other sectors shows great discipline.

Delayed gratification is a muscle that you can grow to serve your future selves. Delayed gratification is the ability to resist the temptation of instant pleasure, it helps you overcome your impulses. Benefits of delayed gratification should be well enshrined in the minds of investors if they want to succeed.

Swadhyay –The simple meaning of Swädhyäy is “to study.” The word Swädhyäy consists of two words, Sva and Adhyäya. Sva means self, and (soul is the self). Adhyäya means study. Therefore, Swädhyäy means a study of one’s own self. Reading, listening to and reflecting on the life elevating teachings is useful in keeping the mind healthy.

Warren Buffett is known to be a voracious reader. Charlie Munger is described by his children as book with legs. They claim to read at least 500 pages per day. One who does not read has no advantage over a person who cannot read. At the end of the day, good investing requires the collation of large amounts of information. It is a pre-requisite for successful investing.

Pratikraman –“Prati” means “back” and “kraman” means “to go”. It means to go back, to reflect and review, to confess and atone, asking for forgiveness from others for one’s own faults of mind, body, and speech in one’s daily activities, and forgiving faults of others and extending friendship to all.

It helps to reflect and introspect occasionally to get rid of our biases. There is no other way an investor can be liberated unless he is free of all biases be it confirmation bias, hindsight bias or even loss aversion biases. There is no way an investor can get liberated if he is not free from ego, as Warren Buffet said it succinctly “Failure comes from ego, greed, envy, fear, imitation. I have success not because I am smart, but because I am rational. One can achieve rationality only by reflecting on one’s own behavior.

There are and will be many moments in our investing journey, when we are blinded by ego in our wins and successes or thundered by negativity and pessimism in unfavorable times but what gets lost in the din is the need for equanimity and calm, as Howard Marks says the superior investor is mature, rational, analytical, objective and unemotional.”

Prayaschiita – Finally repentance, forgiveness, and acceptance of the supreme nature of the markets is the ultimate knowledge. As Seth Klarman said, “We know that we are fallible and must therefore consider the possibility that for every investment we make we may be wrong” Being egoless and accepting our mistakes will be the ultimate forgiveness seek from the markets.

It’s the grueling unforgiving nature of markets, its full of events, scenarios, results, and views. Somewhere between the facts, interpretations and hubris is our basis for a successful investment & as investors and students of the markets, we, perhaps too should follow a similar soul searching “parva” to reflect on our actions and inactions in our journey & quest to become better and wiser investors.

Markets are always full of regrets. I wish I had deployed more in March 2020. I wish I had bought more of my winners. I wish I had gotten rid of my losers sooner. Markets are filled with regrets. Quickly overcoming the regrets and not repeating those “sins” is the way to nirvana in investing.

In conclusion, on the last day it is customary to request forgiveness from everyone we know and meet by saying

“Michhami Dukkadam”

In addition to requesting forgiveness, one must grant forgiveness too. Thus, by forgiving everyone and requesting forgiveness from all we clean and clear our conscience and seek a better approach to investing.

With bowed obeisance,

Michhami Dukkadam to all and wish you all a wonderful investment journey

This market rally reminds us of the movie Shrek and the question, are we there yet? Talking, annoying donkey from the movie Shrek, who kept asking are we there yet? Someday we sure will be.

Are we there yet? Is this the top? Is this the right time to invest? or also in other local street parlance, Yeh level pe market kya lagta hai?

While these questions are not overtly bad, the genesis is, that everyone wants to invest right at the bottom and sell right at the top. The only problem to this that only in hindsight, would one know what is the top and what was the bottom.

Best time to invest in last 2 decades were,

in March 2020 – Covid Crash

in September 2013 – Currency crisis or

in March 2009 – Global Financial Crisis bottom or

in September 2001 – Dot Com Crash Bottom.

So, if those absolute panic bottoms have been 4 in last 2 decades or so, is there a real point in obsessing over it? But mark the common thread amongst all those 4 points, they came amidst crisis. Make it a point to ask the question next time there is a crisis to ask if it is an opportunity.

But as Charlie Munger says and suggest to “Invert always Invert”, The correct question should be, is this a time where we should NOT be investing or remain invested?

Maybe, one would argue, it would have been prudent to not invest

in Jan 2000 just before the Dot Com crash or

in Jan of 2008, before sub-prime blew up the globe or

in Jan 2018, when government policies intended to clean up the economy ended up disrupting it in the short term.

However even in these times, if you move your vision from 1-2 years to 5 years, the outcome still would not have been bad.

If this is the last 2 decades’ history and we can put forward an argument that we are at a better stage in the economy and markets, then we have been at any point in the last decade then ideally, we should not be worried on whether we should be investing now, but rather focus our energies on which are the megatrends developing, where is the value migration likely to happen? which are the companies preparing themselves for the future upheaval? where are the odds stacked in our favour with longer-term horizon?

Conclusion

We cannot have an investing strategy that focusses on the extremes of the market all the time. In fact, focussing on the same can be very counter-productive. Every future market correction seems like a threat and every past market correction was an opportunity in hindsight. If we give up our obsession with finding the extremes in the market it will take away most of our worries.

By Pranav Mehta and Neel Shah

Executive Summary:

The AMC industry in India has seen exponential growth in the last couple of decades. From less than Rs. 1 lakh cr at the turn of the century, the Indian AMC industry today boasts of an AUM of more than Rs. 30 lakh cr. However, by all accounts, we have just scratched the surface in terms of the potential growth of this industry. Buzz words like “under penetration” and “financialization of savings” get thrown around a lot during any discussion on AMCs in India. Via this deep dive into the AMC industry, we try to understand these and many other drivers of the industry. Fundamentally, we try to answer a couple of key questions –

1. Indian AMC industry will grow, but can it grow profitably?

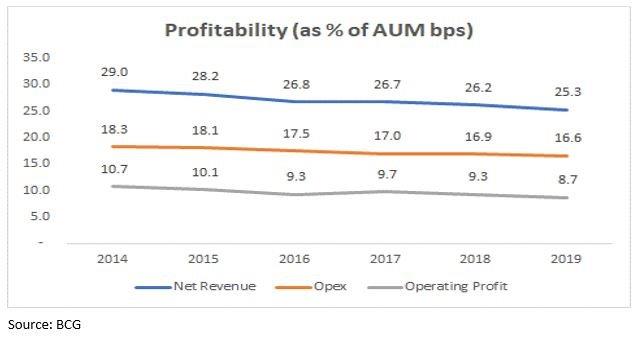

We are confident that this industry can grow at 15%+ for a long time due to a variety of growth drivers discussed in detail in this study. However, certain concerns have emerged in recent years on profitability, especially considering the global experience. Globally, this industry is now at a much more mature stage of growth and grappling with profitability pressures like the rise of passive flows. Our study finds that while the global AMC industry will continue to struggle for profitability, the Indian AMC industry should be able to protect its profitability for few more years at the very least.

2. If yes, what is the best way to play this theme?

Having answered fundamental questions about growth and profitability, we dig deeper into the AMC business model to understand which kind of model to bet on – bank backed AMC or foreign AMC? Large AMC or small AMC? How important is performance, brand, and various other factors in the success/failure of an AMC? Our study finds that scale is very important in the AMC business. Large AMCs backed by bank-led distribution are best placed to grow at a good pace while maintaining best in class profitability.

We believe that this sector has a long runway of profitable growth. Our findings reinforce our bullish view on this space.

DEEP DIVE INTO THE AMC INDUSTRY

What comes to our mind when we think of AMCs in India? Probably a lot of these cool sounding things –

Seems like a very exciting opportunity! But before getting into India, lets first have a look at the key global data and trends.

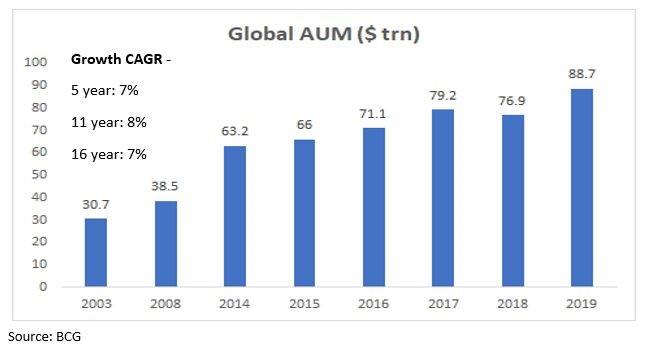

Global Asset Management AUM

The global asset management industry’s Asset Under Management (AUM) has been growing at ~7-8% CAGR. As of 2019, global AUM was more than $88tn vs $63tn as of 2014.

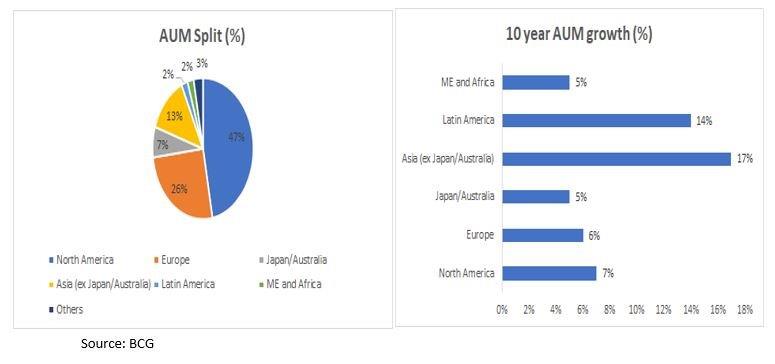

AUM split and growth by key regions

A major chunk of this global AUM is concentrated in North America and Europe. But Asia and Latin America are the fastest growing geographies with Asia growing at 17% CAGR over last 10 years.

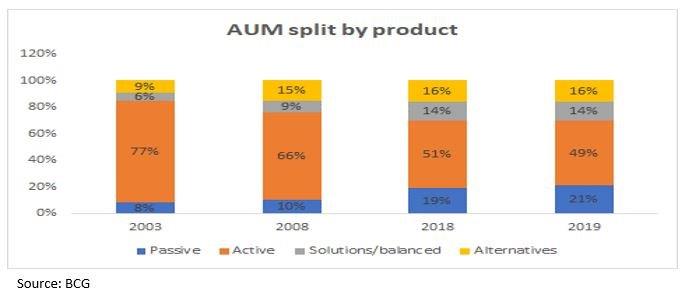

AUM split by product

Over the last 15+ years, the share of passive AUM has gone up from 8% to 21%, whereas the share of active AUM has gone down from 77% to 49%.

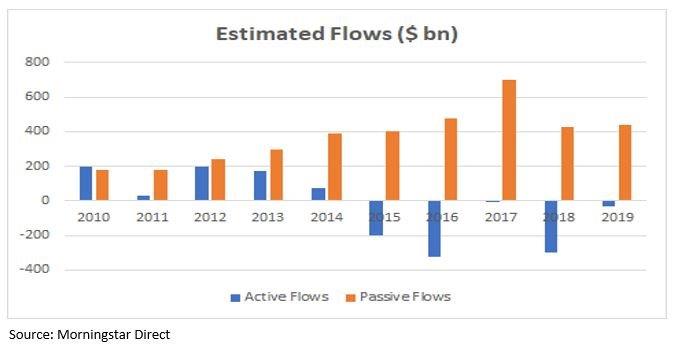

Flows split by style (only for USA)

From 2010-19, passive funds had inflows of $3.8 trn, while actively managed funds had outflows of $185 bn.

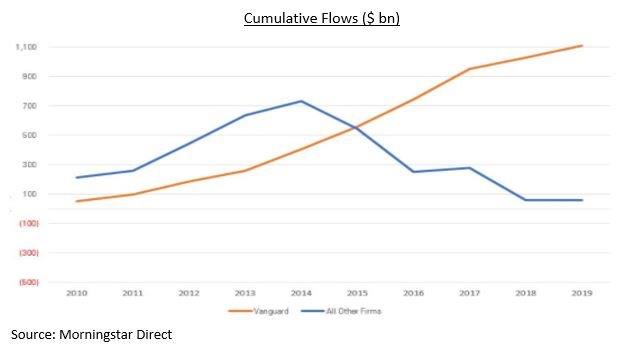

The Vanguard decade

As passive flows in the industry picked up, Vanguard was a big beneficiary. It collected about $1.1 trillion during the decade, while the rest of the industry combined took in less than $100 billion net!!!

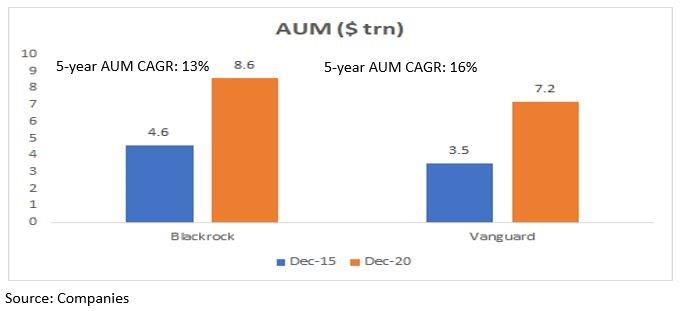

Industry becoming more and more concentrated

Blackrock + Vanguard (top 2 global AMCs) share in global AUM has increased from 12% in 2015 to 16% in 2020.

All these factors have put pressure on profitability…

Note: Based on data of top 100 global asset managers which represents more than 60% of global AUM.

AMCs typically earn significantly lesser fees from passive funds as compared to active funds. So, with huge flows seen in passive funds, profitability of AMCs has been under immense pressure in the last decade.

This has led to consolidation in the industry. In recent years, many M&A deals were observed in the industry with many big players like Oppenheimer and Eaton Vance being bought out.

Summary of key global trends

– Overall AUM growth rates have been at ~7-8% for the last 15-20 years. – Asia (ex-Japan and Australia) and Latin America are the fastest growing regions with 14-17% long term growth. – Shift from active to passive investing is the megatrend in the industry. The numbers for passive flows in the last decade are simply stunning! – This has led to significant pressure on profitability of AMCs due to downward pressure on fees, leading to consolidation in the industry. – Top AMCs like Blackrock and Vanguard have capitalized on the passive trend to grow much faster.

OVERALL, IT SEEMS THAT GLOBAL AMCs’ P&L IS UNDER SIGNIFICANT STRAIN. PROFIT GROWTH IS EXPECTED TO BE MUCH LOWER THAN AUM GROWTH.

Considering these global trends, should we still be as excited about the India opportunity?

Indian AMC Industry

Historical Growth

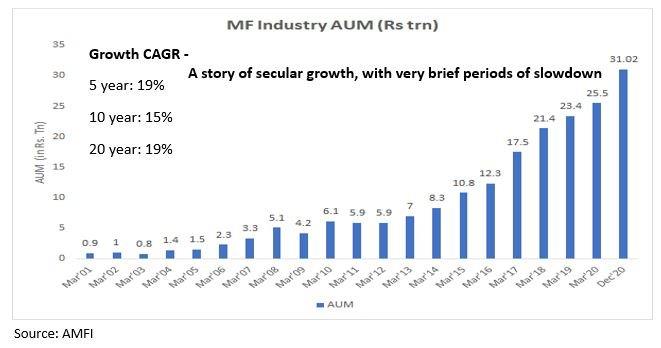

Indian MF AUM has grown at a healthy pace in the last 20 years with very brief periods of slowdown. Over the last 5 years it has grown at 19% CAGR to reach Rs.31tn which was a mere Rs.6tn in 2011.

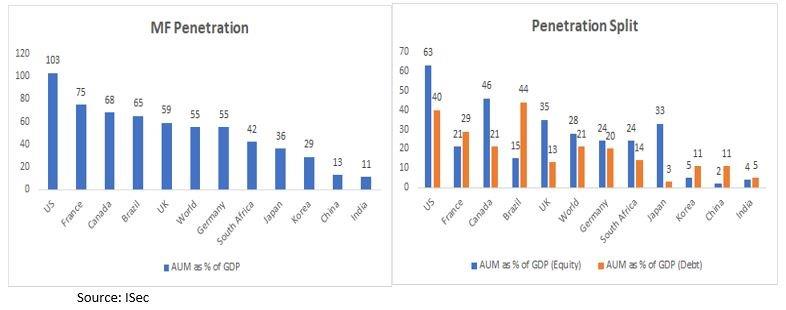

But despite this growth, the industry is still underpenetrated.

India’s AUM to GDP ratio is one of the lowest in the world.

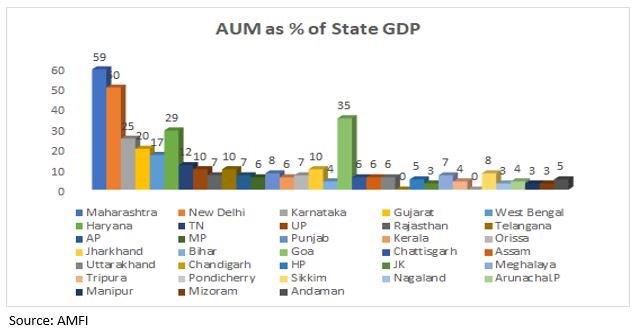

Under-penetration (state wise)

An analysis of state-wise penetration data reveals that only a handful of states in the country are well penetrated. Most of the smaller states fall way below the national average.

Various accounts

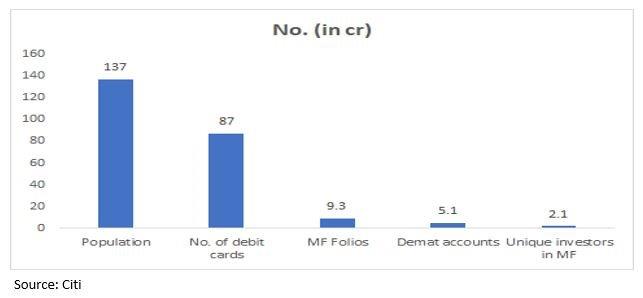

India has just 2.1 cr unique MF investors (9.3 cr total MF folios). We have barely scratched the surface! In India, under-penetration is combined with high savings rate – a good combination to have!

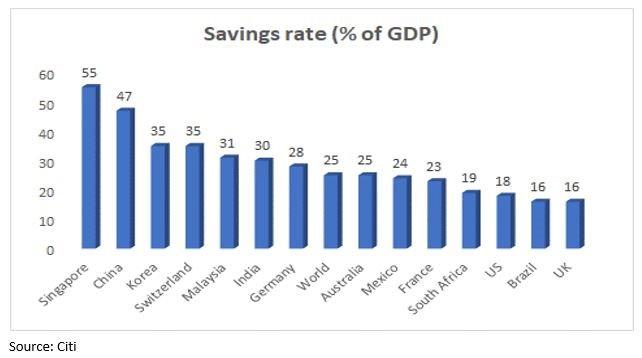

Savings rate

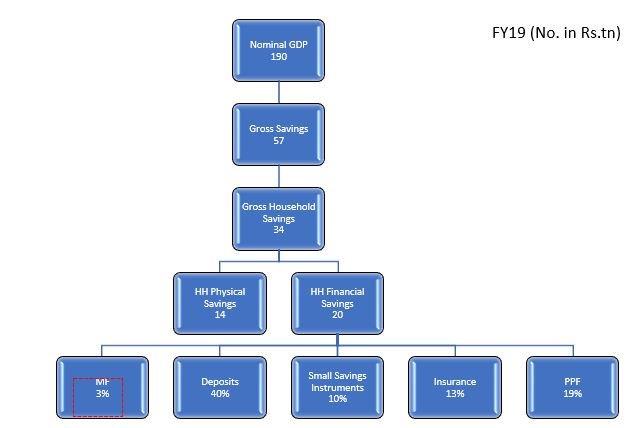

But how does India save? For illustration, let us look at FY19 nos.

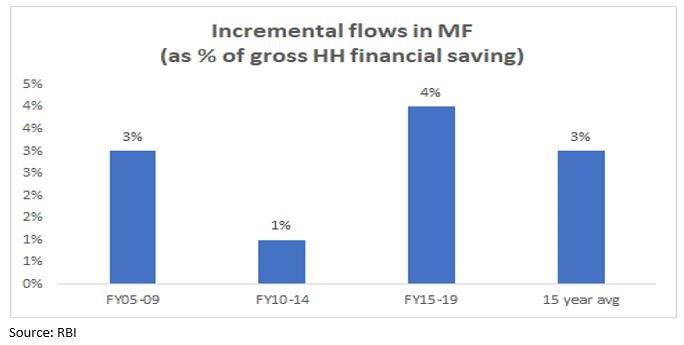

In FY19, ~58% of gross household savings flew into financial savings. However, only 3% of household financial savings found its way into MFs.

Financialization of savings – Cyclical or structural?

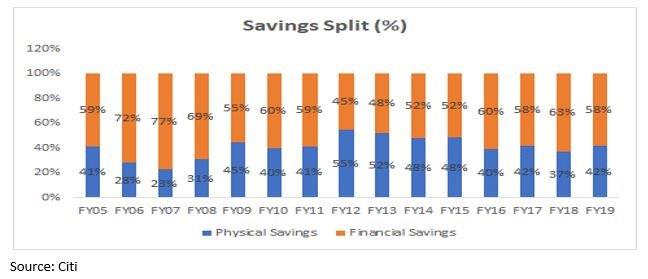

The share of physical and financial savings in the total savings pie keeps fluctuating, reflecting a cyclical nature. To illustrate, share of financial savings in total savings was as high as 77% in FY07, as low as 45% in FY12 and settled at 58-80% in last few years.

There is a bigger opportunity out there for MFs – taking share away from other financial assets.

Big opportunity – taking share away from other financial assets.

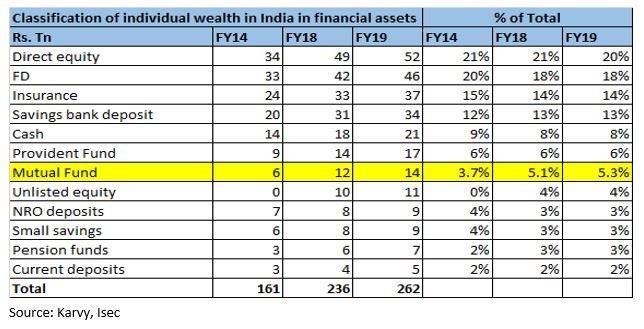

In the last 15 years, only 3% of incremental gross household financial savings has flown into MFs and only 5% of individual financial wealth in India is in MFs.

Under-penetration + high savings rate + scope for market share gains = long growth runway for AMCs. The above factors plus a historical 1.4x multiplier on nominal GDP growth gives confidence of 15%+ long term AUM growth. However, near term cyclicality will always be a factor.

But what about the profitability question? What about the global megatrend of rising passive/ETF flows and lower fees?

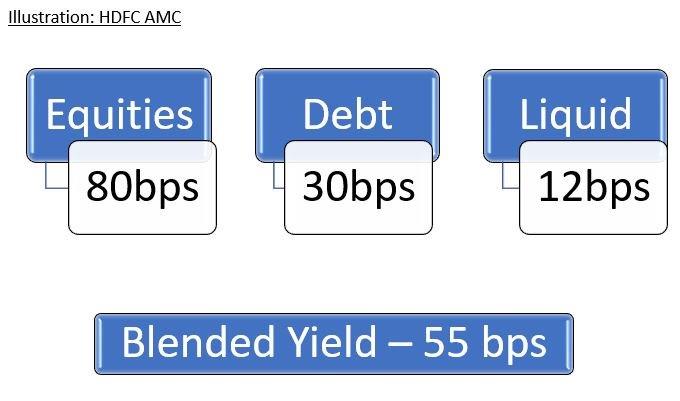

To answer these questions, first let’s understand how does an AMC earn fees?

Active equity funds generate the highest fees while liquid funds generate the lowest of the three. Passive funds have significantly lower fees across all categories.

Impact on profitability can come from –

– Rising share of passive/ETFs – Mix change from equity towards debt or liquid – Any cut in Total Expense Ratio (TER) for equity funds

Let us take a look at these factors one by one…

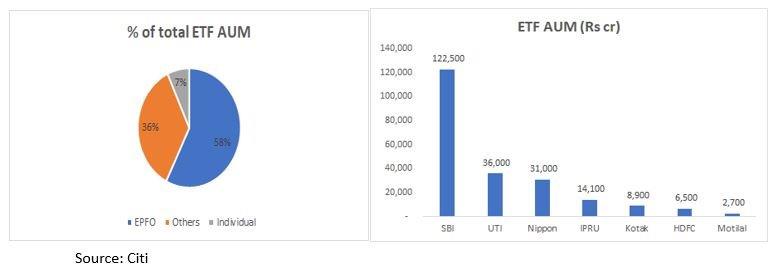

– Growth of ETFs in India

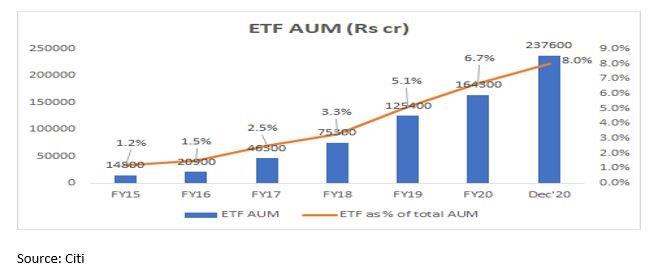

ETF AUM has grown exponentially to Rs. 2.3 trn (~8% of total AMC AUM)

Scary? Cause for concern? Not really.

In India, ETF AUM is restricted largely to EPFO and other wholesale (primarily Government) channels. EPFO can invest 85% of its annual deposits in debt instruments and the remaining 15% in equity invested via ETFs. SBI MF and UTI MF run the EPFO mandate and share AUM in the ratio of 3:1.

Pure retail flows into ETF are miniscule and not gaining too much popularity as of now.

ETF AUM as % of AUM is significant for SBI MF (27%), UTI MF (22%) and Nippon (15%)

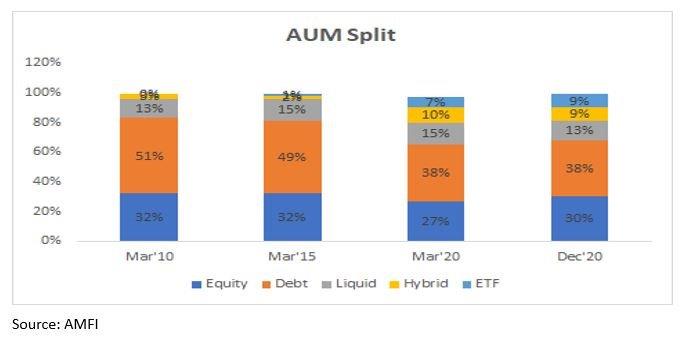

– Equity mix has been steady.

Share of equity has remained broadly stable over long term, short term fluctuations cannot be ruled out.

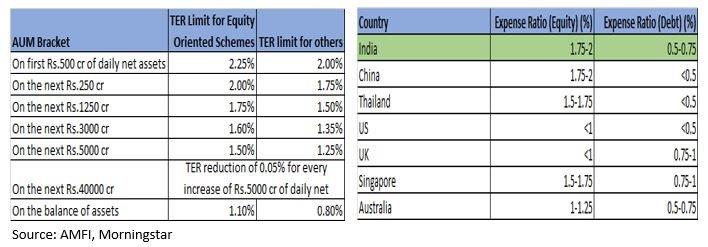

– History of TER tweaks by SEBI

– 2009 – Removal of entry loads on all MF schemes by SEBI – 2012 – SEBI allowed AMCs to charge incremental expenses of 30 bps on new fund flows from B15 (beyond top-15) cities. – 2018 – Reduced a 20bps permissible charge in case of mutual fund schemes where exit load is not levied to 5bps. Issued revised terms and definitions and permitted additional TER of up to 30 bps for inflows from B30 cities instead of B15. All commissions to be paid from the scheme P&L and distributor commissions to be only on a trail basis (no upfront commission). – 2019 – SEBI cut the TER chargeable to investors.

Not all tweaking by SEBI has been negative. Generally, they prefer to bring pricing down only after size of the industry has grown multifold. With the last round of TER cut happening in 2019, it is expected that the regulator will not engage in major pricing action for the next few years.

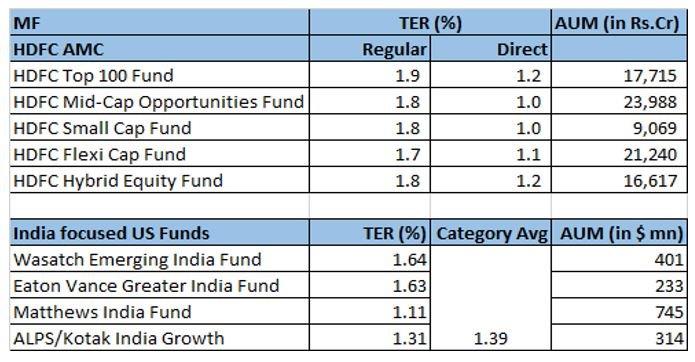

Is India’s TER higher than global standards?

India’s TER is in line with most developing countries. Some developed countries like US and UK have significantly lower TER. But if we look at India-focused funds in US, we see that the TER for these funds is in line with funds in India.

High pricing power>>TER cuts have been passed on

In any case, whenever SEBI has cut TER for the industry, most of the AMCs have been able to pass it on in the form of lower distributor commissions.

Risk: Threat of new competition/disruption

– In recent months, we have seen a plethora of companies applying for AMC license – Helios Capital, Alchemy Capital, Wizemarkets Analytics, Bajaj Finserv, Zerodha, Samco Securities, NJ India Invest etc. Some of the new applications follow SEBI’s move to ease the profitability criteria for setting up an AMC. In December 2020, SEBI said sponsors which don’t fulfill the profitability track record can still set up a fund house, provided they have a minimum net-worth of Rs 100 crore, instead of Rs 50 crore that is otherwise required. Some other companies like Groww and Flipkart founder Sachin Bansal’s Navi Technologies have taken the inorganic route to obtain a license.

– With the entry of these players, the competitive scenario is set to intensify. The new entrants will try to disrupt the distribution as well as fund management model prevalent in the industry. Given that active management is already a crowded market and the nascent stage of passive management in India, some players like Zerodha plan to exclusively focus on passive funds. Some degree of compression in yields due to new competition cannot be ruled out. However, in event of yield pressure, the distributor category will be more vulnerable given the AMCs’ dominant position in the industry chain. Also, incumbents have advantage of scale. As seen later in this study, it is very difficult to turn an AMC profitable at a smaller scale of AUM. That challenge awaits all the new entrants. Moreover, new entrants will expand the existing market which can in turn prove to be beneficial to the incumbents. For example, 65% of investors on Groww’s MF platform are first time investors.

Growth + Profitability is good. So kya leneka? By that, we don’t mean to give a stock tip. The focus of this study is to understand within AMCs, which is the right model to bet on – bank backed AMC or foreign AMC? Large AMC or small AMC? For that, it is important to first understand the industry landscape.

Industry landscape

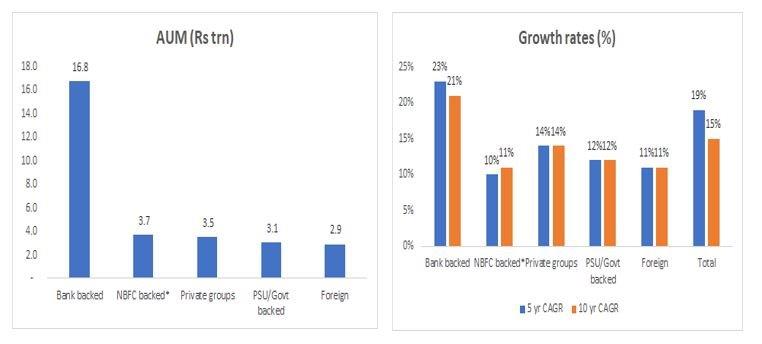

There are currently 42 AMCs operating in India. By ownership, they can be broadly split into –

*For this calculation, Nippon MF has been considered as NBFC backed AMC

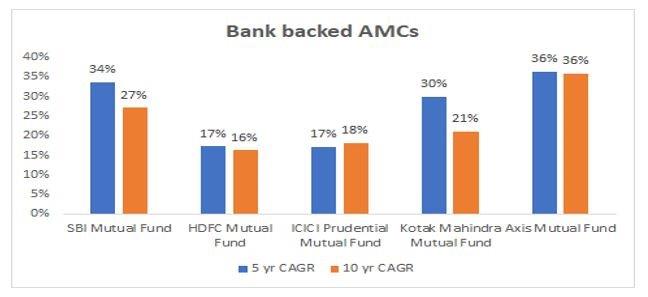

Bank backed AMCs have grown the fastest; led by distribution benefits and strong brands. All other groups have grown at similar rates and are much smaller than bank backed AMCs. All other categories are in Rs. 3-3.5 trn range – in other words even smaller than one HDFC AMC!

Growth in bank backed AMCs has been broad based. Axis has been the one with highest growth rate albeit with a lower base than its peers.

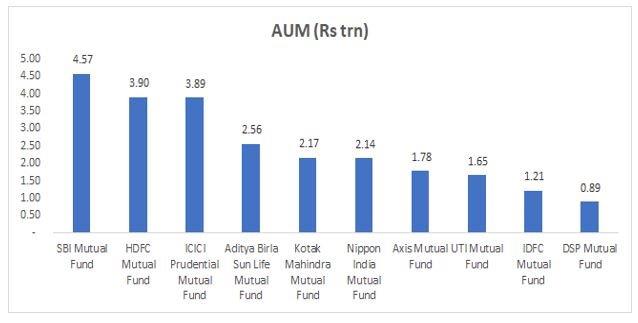

Top 10 AMCs dominate the market

Share of Top 10 AMCs has improved to 83% in 2020 vs 78% in 2015. Big players have grown bigger over the years.

What are the key drivers of growth?

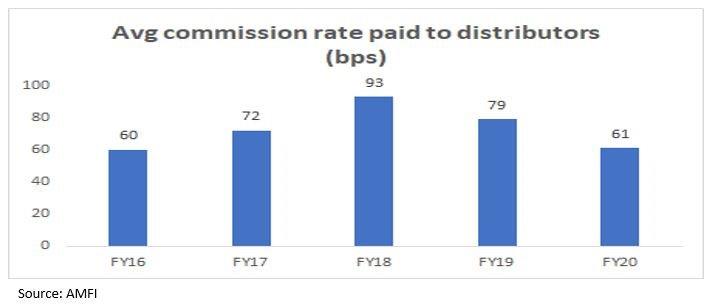

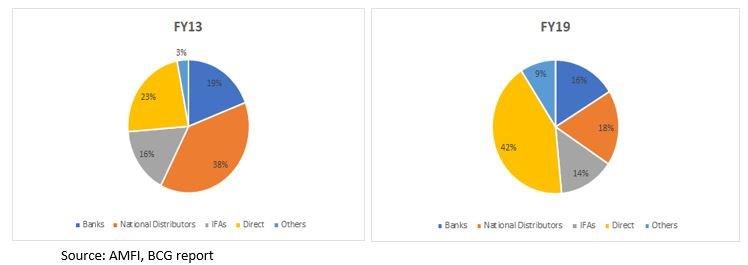

– Distribution

In recent years, Direct as a channel has grown by leaps and bounds whereas the share of other channels has come down. One thing to note here is that AMC profitability is not materially different in Direct vs Regular model. The distributor fee in the Regular model is passed on to customers in the Direct model in the form of lower TER. As Direct gains more share, it is the distributor that stands to lose the most.

– Brand – Performance

How important is performance?

In the last few years, Axis MF and Mirae MF have been the standout AMCs in terms of scheme performance. While Axis MF has grown at a healthy pace, Mirae MF has been the fastest growing AMC (organically) in the last 5 years.

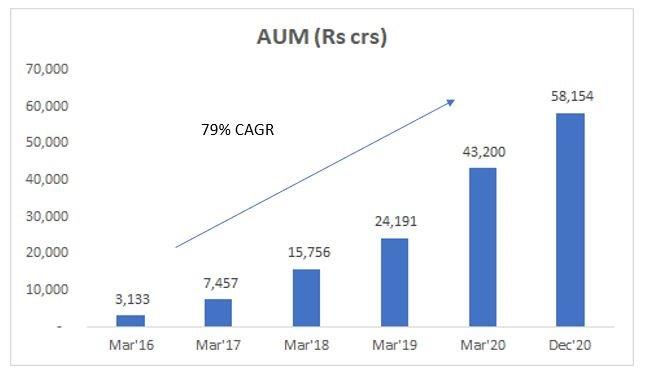

Case Study – Mirae Asset Mutual Fund

Mirae’s schemes have been in the top quartile in terms of performance across most categories in the past few years. Such level of stellar performance has enabled them to grow their AUM at a rapid 79% CAGR since 2016. Mirae is a rare example of a foreign AMC succeeding in scaling up their operations to a decent level in recent years.

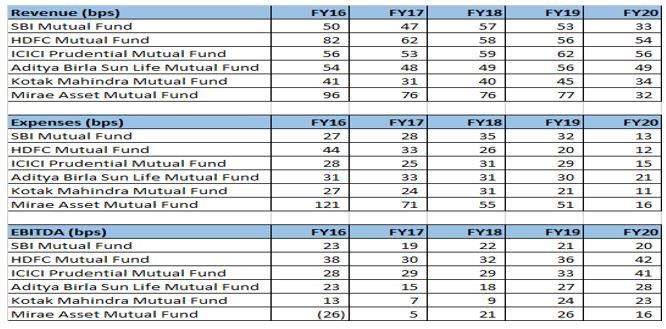

Mirae vs Top 5 MFs

While Mirae has seen a major improvement in profitability, it is still much lower than the Top 5 AMCs’ profitability (especially HDFC and ICICI MF). The difference is on 2 counts – net revenue realization is much lower for Mirae presumably due to higher distributor payouts than large AMCs and due to scale benefits, larger AMCs have much better cost absorption. If this is the differential in profitability with large AMCs for the best performing “small” AMC, then what about other small AMCs?

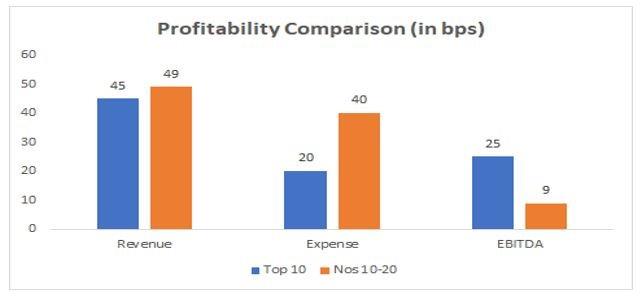

Avg profitability – Top 10 vs No10-20

Smaller AMCs command a slightly higher fee on average (maybe due to better equity mix) but have significantly weaker cost absorption as they lack the advantage of scale.

Conclusion: Size matters…. a lot!

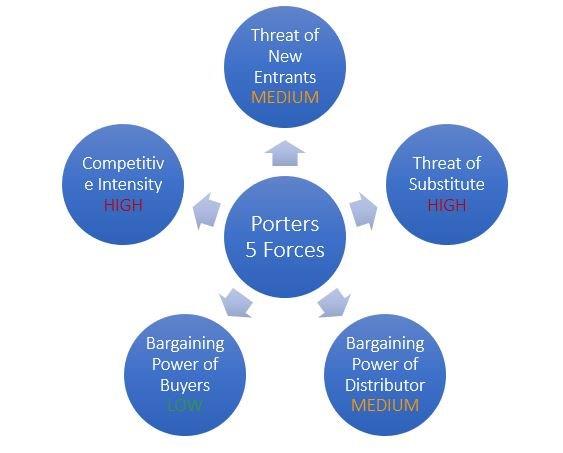

Porter’s Five Forces

Following are the key takeaways from a survey we conducted amongst distributors for this study –

Does it still make sense to sell MFs?

Yes. Still many opportunities to make good commission.

Which MFs are most popular/easily sold?

Despite underperformance, HDFC still remains most sought after. Additionally, there are always flavours of the season – Axis, Mirae.

Do clients care which MF you are investing in?

Most of them do care. Lot more push required for selling smaller/new funds.

What points do you consider while deciding which MF to invest in?

Commission, consistency, fund manager, brand

Which AMCs give highest commission to distributors?

Smaller AMCs like Mirae, Invesco continue giving good commissions as in the past. Least sharing done by HDFC, ICICI but those AMCs have biggest customer pull.

Does rising trend of direct investing pose a big problem for distributors?

Not really. Many a times customers who opted for Direct have moved back to advisors after having bad experiences.

Which MF does a client prefer – best brand or best performance?

Advisors generally create a portfolio with mix of both.

Any demand of ETFs from retail investors?

Sporadic enquiries. Nothing major.

Valuations

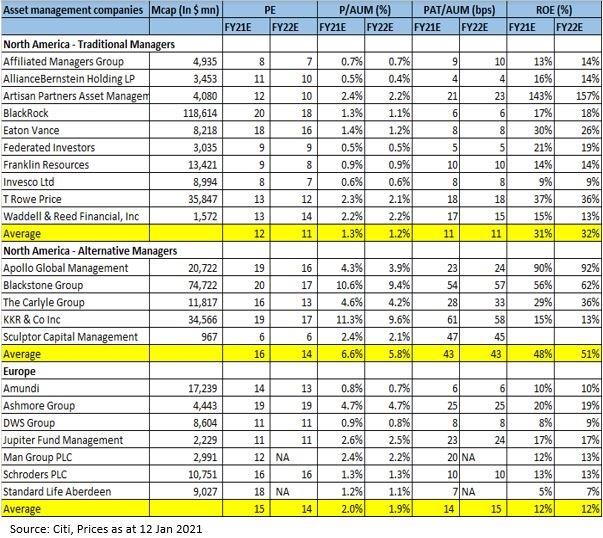

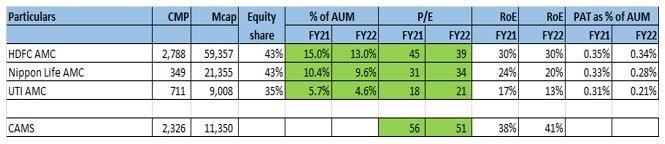

Global Valuations

India Valuations

Global players command a significantly lower valuation as compared to Indian AMCs.

Why India deserves a premium valuation to the world?

– Higher growth (19% CAGR vs 7% CAGR for the world) – Under-penetration – Higher current profitability – Fewer headwinds on future profitability

Conclusion

– Global AUM growth is 7%. But profit pool growing much slower. – Indian AMC industry is set for strong growth of 15%+ for the next decade. However, growth will not be linear and prone to cycles. – Indian AMCs are in a much better position to protect their profitability than global peers. – Within Indian AMCs, the model to go for is large AMCs with strong brand and distribution backing like bank backed AMCs. – Valuations look optically high for Indian AMCs. However, the premium to global peers seems justified due to superior growth and profitability.

In Dec 2020, Indian Investing Conclave hosted our MD & CIO Mr. Ravi Dharamshi, who spoke about about CPaaS (Communications Platform as a Service), an opportunity.

Quick Summary:

A CPaaS is a cloud-based platform that enables developers to add real-time communications features to their own applications without needing to build back end infrastructure and interfaces.

It is a niche segment within technology, even though we have few companies in this segment which are listed.

Investment Hypothesis in CPaaS companies (growing at 40%) – Crossed the technology adoption chasm – Huge addressable opportunity – Industry growth estimates 30-50% – Profitable Unit Economics – Cash Generating – Incremental cost of customer acquisition is very low.

Seven-dose potent VACCINE for the Indian Economy

Several pathogens had infected the Indian economy – namely consumption dip, fragile jobs ecosystem, pandemic-led social spending, reduced revenues, and fiscal-deficit tight rope walk.

A plan to combat these was well laid out in the first paperless Union Budget, through what is akin to a 7-dose “VACCINE” shot.

While the economic hygiene had been maintained all through 2020 by the Reserve Bank of India’s monetary policy, the penultimate boost to the frail economy has come in the form of Budget 2021-22.

V-shaped Recovery in sight

The Economic Survey has indicated a V-shaped recovery in the next FY 2021-22 even as an economic contraction of 7.7% has been forecasted for the FY 2020-21.

Pushing the growth multiplier rather than stoking consumption with steroids has been high on the Government’s radar.

While the easy way out could have been to induce consumption through tax rebates and money in the hands of consumers, the challenging path of concrete growth inducers such as infrastructure and investments spends were adopted.

Atmanirbhar Bharat

Taking major stride towards the aim of self-reliant India, a cushion worth Rs 1.97 lakh crore was offered to the manufacturing sector to spur domestic facilities. The electronics, automobiles and auto ancillary, telecom, pharma and textiles industries would be able to utilise the amount over a period of five years.

Additionally, seven large Mega Investment Textiles Parks (MITRA) would offer a playground of sorts to nurture global export businesses through the plug and play model over the next three years.

Capex-led revival

There is a tectonic shift in the mindset of the NDA Government that is ready to bite the risk-bullet. It has shed the crisis-management garb and adorned the capex-investment outfit, ready to tackle economic contraction head on. It is unperturbed by the additional weight of fiscal deficit.

Enhancing FY 2022 capital expenditure allocation by 26% year-on-year, the Government would spend a whopping Rs.5.5lakh crore more on creating assets like roads, railway lines, factories, ports. Spearheading the infrastructure creation drive would be the freshly created Development Finance Institution with a bounty of Rs 20,000 crore, which emphasis the thrust on physical assets.

Cleaning-up Act

There are strong indicators from the Government that it is looking to clean up its books winding down to FY 2026. The first indicator is the decision to bring all the food subsidy on its books rather than the funding through Food Corporation of India, which was an off-balance sheet funding mechanism.

Also, reliance on off-balance sheet funding through National Highways Authority of India and other extra-Budgetary resources has been reduced.

Apart from, the cleaning up drive, the Budget calculus seems to have undergone a shift toward moderate projections keeping in view the growth estimates. As a result, the estimations drawn in the Budget 2021-22 have a flavor of credibility to them.

Backing this claim is the fact that the divestment targets for FY 2021-22 have been judiciously placed 17% lower than the previous year. Gross tax revenue projections too have been pegged in line with 14.4% year-on-year rise in nominal GDP.

Infrastructure

Both physical and financial infrastructure augmentation would be carried out through various moves.

Capital expenditure has always been restricted to 13.5% of the GDP. But the infrastructure-push message has been made loud and clear with a significant allocation of 15.6% of GDP to expenditure, thereby dampening even the inflation worries.

Equity infusion of Rs 20,000 crore has been allocated for public sector banks, even as a new asset reconstruction company would take over bad bank loans. These steps are vital to improve the access to credit.

Divestment and monetization of operation assets through Infrastructure Investment Trusts would offer the Government additional strength to fund various initiatives.

No tax hikes

Similar to all the four Budgets presented after a year of contraction, the Finance Minister steered clear of any income tax raise. No hike was proposed in personal, corporate taxation or even indirect taxes. Nasty surprises in cess, capital gains or wealth tax too were kept at bay.

The move was well thought to avoid any hurdle in the way of consumption. Contemporary ways to fill the revenue gap were thought of in the form of additional borrowing, divestment, increase in insurance foreign direct investment limit and zero coupon bonds.

The sensitive side of the Government came to the fore with the advance tax alteration with respect to dividends and even offering foreign portfolio investors a reduced lower Treaty Rate for dividends income tax.

Expansionary not austere

There was a realization through various allocations that even as the fiscal deficit would expand, the purse strings will have to be loosened for growth. Developed nations too have struggled with austerity.

Back home, the Finance Minister set sights on fiscal deficit target of 6.8% of GDP getting rid of the shackles of the 3% fiscal deficit target specified by the Fiscal Responsibility and Budget Management Act. It reflects the intentions that fiscal consolidation path would extend a little longer.

The deviation in the fiscal deficit roadmap had already been trigged in FY 2020-21 owing to the pandemic-led growth infusion, which pushed the figures to 9.5% of GDP. Hence, the audacious attempt at spurring growth – even if it took longer to achieve 4.5% fiscal deficit – was undertaken.

This move would have an expansionary effect as the investment would have a spill over across multiple sectors due to improvement in employment opportunities and in turn money in the hands of individuals.

Conclusion

Just like the six pillars that the Budget 2021-22 was placed on, the seven key VACCINE doses are pertinent.

To conclude, the medicine in the right dosage will have to be administered if the economy has to bounce back and hurl past the reach the $5-trillion GDP mark by 2024-25. There could be certain adverse reactions (read: ballooning fiscal deficit). But the prescription seems to be based on the correct prognosis of what Bharat needs in the long run.

Disclaimer, Disclosures & Important notices:

This document prepared by ValueQuest Investment Advisors Ltd, is meant for the sole use of the recipient and not for public circulation. This document should not be reported or copied or made available to others, either in part or full. The information contained herein is obtained based on internal data and publicly available information and other sources believed to be reliable.

ValueQuest does not claim or warrant the accuracy, correctness or completeness of the data mentioned herein. As such, this document should not be relied upon for any purposes including investments in any security. This document is for personal information only and does not constitute an offer, invitation, or inducement to invest in any security whatsoever. ValueQuest or any of its employees are under no obligation to update the information contained in this document. As permitted by SEBI regulation, ValueQuest and its affiliates, associates, officers, directors, and employees, including persons involved in preparation of this document may: (a) from time to time have a long or short position, or buy or sell, any of the securities of any company mentioned herein or otherwise; or (b) be engaged in any other transaction involving such securities. Performance related information provided in this document is not verified by SEBI. Past performance is not a guide for future performance.

Investment in equities involves substantial risk including permanent loss of capital (in whole or in part) and hence may not be suitable for all investors. The statements contained herein may include statements of future expectations and other forward-‐looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible / liable for any decision taken based on this presentation. Readers should before investing make their own investigation and seek appropriate professional advice. Investments in Securities are subject to market and other risks and there is no assurance or guarantee that the objectives of any of the strategies of the Portfolio Management Services will be achieved. Clients under Portfolio Management Services are not being offered any guaranteed/assured returns.

The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe any such restrictions.

Please read the following carefully and select your residency jurisdiction

*If you access this website by giving false declaration, you shall be solely liable/responsible for any adverse consequences suffered, legally as well as financially, pursuant to use of any information contained in this website.