US markets are living through unprecedented times. Everyone is feeling giddy. There are so many mini bubbles: Tesla, SPAC, Bitcoin, SaaS.

• Exponential price growth • Leading to fund raising • New Investors who do not know what they are doing. • Early Investors and insiders are selling or looking to sell. • Old economy stocks are also soaring as they try and get piece of the new shiny thing. • Crazy price movements in unheard of names with no connection to the fundamentals – Signal, GameStop, AMC.

If it looks like a bubble, feels like a bubble then it must be a bubble right?

• Little-understood technology • Unrealistic promises of endless revenues • Scores of small-time investors • Difficult to understand and value • People buying only because it is going up in value

Is this just a bigger bubble, barrelling towards a louder pop?.

However, the thing about bubbles is nobody knows how big they will get before they pop. Nobody knows the precise moment or the precise reason for the bubble to pop.

As has been our view, Covid is not the needle that pricks the bubble, in fact it has fuelled it even more, Now it is pretty self evident. Unprecedented global coordinated stimulus provided to the world economy is going to create more and bigger bubbles. To Learn more and make an informed view yourself.

Please go through the ValueQuest Webinar on Bull Market or Bubble:

Dear VQ Investors,

From the staggering drop in equity amounting to 40% in just a months time back in March, to a recovery to all-time high levels, 2020 has been the year of the volatility and unpredictability. In the context of financial markets, historical significance, and lessons it taught us this year, 2020 is right up there with 1929 and 2008.

It is time for an honest mark-to-market in 2020. A moment to look back and reflect.

2020: The year of reflection

In March 2020, the world came to a stand-still. But we strongly believed that if we stayed true to our process, if we focused on building our conviction in the investee companies, if we focused on watering our flowers and weeding out the dead wood, and if we focused on staying in the game long enough, then our efforts would be rewarded.

What does not kill you only makes you stronger is an adage that applies well here. That is exactly how our portfolio displayed resilience, and now, it is thriving in the much-improved investment scenario.

2020: The year of resilience

We had to be resilient over the past 10 months. Amongst the uncertainty and market volatility, compounded by the global economy that plunged into deep recession, it was imperative that we stood our ground and rode out the storm.

The performance of our portfolio affirms our notion. After being resilient, it is now thriving in today’ investment scenario

2020: The year of re-awakening

As the pandemic struck, we decided to focus on rejuvenating the portfolio with stocks that would drive returns in the changed world.

Chemicals & Pharma were identified as the sectors that would benefit from the distrust towards China, as the world looks for alternatives. Agriculture & Rural economy were identified as segments of the economy that would bounce back the fastest. Technology & Telecom were identified as the sectors that would thrive in this new, digitally driven world.

2020: The year of developing perspectives

The Indian economy has been in repair-mode for a major part of the last decade. Indian corporates have been in de-leveraging mode, and corporate profits to GDP has been at a decadal low. Having this perspective tells us that what happened in March was a culmination of all that was bad; it precipitated what was predestined in a shorter time frame. Once you have the confidence to say that we have reached the point of maximum pessimism, it becomes imperative that we turn positive. Subsequent earnings of corporates in Q1 FY21 and Q2 FY21 are a testament to the fact that now the analysts are behind the curve in terms of earnings. This is the first time in the past 7 years or so that there have been more earnings upgrades than downgrades in our universe of stocks.

Point of Maximum Pessimism

March 2020 was the point of maximum pessimism as one by one we gave up on govt policies, market returns, portfolios, businesses and even life. That is when the seeds of new bull market are sown.

2020: The year when a new bull market was born

Bull Markets are born in pessimism, grow in skepticism, mature on optimism, and die on Euphoria. We strongly believe that we are still moving from the pessimism phase to skepticism phase and we are no where close to the Euphoria that some would believe.

Here’s wishing you the best of health, wealth and peace of mind that life has to offer in 2021 and beyond.

Thank you.

ValueQuest

Disclaimer, Disclosures & Important notices:

This document prepared by ValueQuest Investment Advisors Ltd, is meant for the sole use of the recipient and not for public circulation. This document should not be reported or copied or made available to others, either in part or full. The information contained herein is obtained based on internal data and publicly available information and other sources believed to be reliable.

ValueQuest does not claim or warrant the accuracy, correctness or completeness of the data mentioned herein. As such, this document should not be relied upon for any purposes including investments in any security. This document is for personal information only and does not constitute an offer, invitation, or inducement to invest in any security whatsoever. ValueQuest or any of its employees are under no obligation to update the information contained in this document. As permitted by SEBI regulation, ValueQuest and its affiliates, associates, officers, directors, and employees, including persons involved in preparation of this document may: (a) from time to time have a long or short position, or buy or sell, any of the securities of any company mentioned herein or otherwise; or (b) be engaged in any other transaction involving such securities. Performance related information provided in this document is not verified by SEBI. Past performance is not a guide for future performance. Investment in equities involves substantial risk including permanent loss of capital (in whole or in part) and hence may not be suitable for all investors. The statements contained herein may include statements of future expectations and other forward-‐looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible / liable for any decision taken based on this presentation. Readers should before investing make their own investigation and seek appropriate professional advice. Investments in Securities are subject to market and other risks and there is no assurance or guarantee that the objectives of any of the strategies of the Portfolio Management Services will be achieved. Clients under Portfolio Management Services are not being offered any guaranteed/assured returns.

The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe any such restrictions.

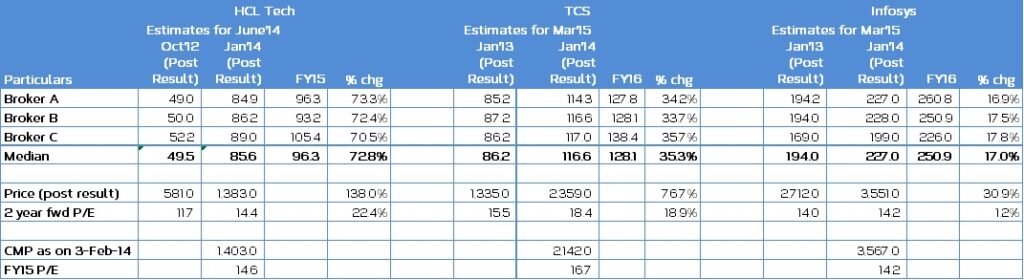

Indian Technology sector has been one of the best performing sector in Indian market. TCS, which is the largest market cap company in India has been a 7x-bagger over last 5 years. Can the sector possibly delivery absolute returns even from here? Is the sector overvalued? Is the re-rating of the sector complete?

We believe not!!

In India IT is one of the few sector which is researched to the minutest levels of details by the research community. Further, there is also a detailed level of corporate updates and growth guidance, post every quarterly earnings from the company’s end. Despite being rigorously tracked sector, the analyst community have not only failed to gauge the earnings estimates, but the magnitude of the miss in the earnings is also quite stupendous esp. for HCL Tech (as mentioned herein below).

In our study the point we are trying to make is, it is the earnings growth registered by the IT companies which have the seen the stock price increasing in the range of 30-175% over a 12-15 months span rather than re-rating of the PE multiple.

As seen from table 1, though HCL Tech stock price increased by 138% from the period between Oct’12 and Jan’14, it was largely driven by change in earnings growth for FY14 which was revised upwards by 73% and mobile casino balance by re-rating in two year earnings multiple by 22% because of the strong earnings performance.

Similarly for TCS price increase of 77% in last four quarters is largely the function of earnings upgrades by 35% and balance due to change in two year multiple by 19% on sustained earnings performance.

However for Infosys, the price increase of 31% in last four quarters is only led by change in earnings upgrades which were revised upwards by 17% wherein the two year fwd multiple was largely the same at 14x.

Key points from the above observations

To give the benefit of doubt to the analysts, hindsight is always 20-20. Instead of being critical on other’s work the observations we are trying to make are:

– Analyst estimates (irrespective of their intelligence, network or foresight) are never accurate.

– Companies themselves rarely are able to visualize the coming change until it is well underway.

– We believe re-rating witnessed in IT sector is still partial. Majority of the stock price move has been earnings momentum.

– Real re-rating will happen the day when investor community starts believing that the growth trajectory can move from current 12 – 16% for most companies to 17 – 20% on a sustained basis.

to put it in perspective, Indian technology outsourcing companies are valued at a higher multiple than their counterparts in US. However, In a bullish market, large established business growing at 15% with clean balance sheet, 30% ROCE and reasonable visibility of future would not have been trading at 15-17 PE multiple.

What should an Investor do? Focus on drivers of business growth and margins rather than movement in stock price

An investor should focus on drivers of growth and profit rather than the magnitude of the profits or the movement in prices:

o US economy growth rate to determine the growth in discretionary spending

o Indian companies ability to gain market share in the Global IT spend remains the biggest driver till date

o Increasing outsourcing from European countries

o Rupee movement vis-à-vis USD, GBP & Euro

o Cost control measures and other operational efficiency (increasing utilization)

Finally to sum up, we strongly believe that Investing is more an act of wisdom rather than knowledge.

Since 2009, Flipkart has raised over $550 million and the latest fund raising is a telling tale of how Flipkart is the runway leader in e-commerce.

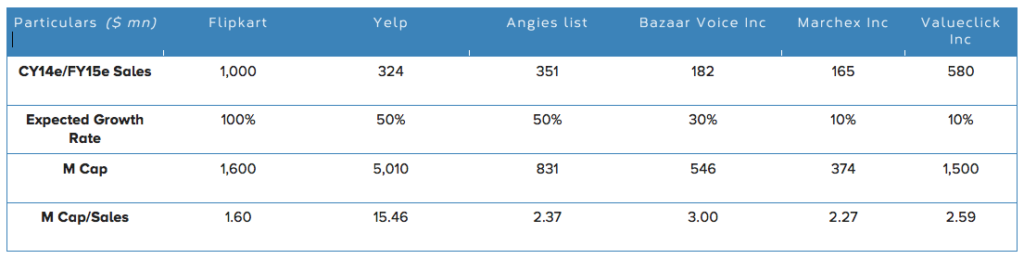

Flipkart raised total $360 million from the fifth round of funding, which values the company at $ 1.6 billion. Flipkart strictly has no comparable in the listed space. But its relevant enough to give the contrast in the buoyant valuations of private equity space vs the depressed valuations of secondary market. We have attempted to compare it with the off-line retailers and Just dial (which is the one of the two listed e-commerce plays available)

Flipkart v/s Offline Retailers: Stark difference in Valuations

Flipkart is worth more than the total market cap of all top 3 listed Indian retail companies Future Retail, Shoppers Stop & Trent combined. These companies have a Market cap close to Rs 9000 crs whereas Flipkart is valued at Rs 9600 crs. To compare apple to apple, off-line retailers have a big debt and hence we should compare Entireprise Value (Market Cap Debt). Enterprise Value of these 3 companies combined on consolidated basis comes to around 14,500crs. Flipkart benchmark valuations have been established by suave private equity players, who we assume have not been euphoric while valuing the company. Why is it that PE players want a piece of Flipkart while the entire listed space goes for a song?

Growth

Flipkart sales grew by a robust 178% in FY2013 to Rs. 1345 crs. There has been a strong growth in Sales. On the other hand, retail sales in the economy have been decelerating.

Profits

Flipkart has succeeded in building a scale and looks like an early winner in E-commerce, which is an emerging growth area. So even though currently the losses have increased for them from 62crs to 192crs, business has reached a stage from where the operating leverage will kick in and it can be expected that they will turn in a profit over next 2-3 years.

Business Model

Flipkart is a pioneer in Ecommerce and early success thanks to its aggressive pricing, innovative marketing and cash on delivery model. India is a young and aspiring country and young Indian”s preferences are going to be to increasingly shop online. E-commerce never took off initially in India due to less penetration of computers and online casino dgfev internet and averse-ness to buying online with credit cards. With the explosion of mobile telephony and penetration of smart phones and 3G, M-commerce has become a reality. Cash on delivery is an important enabling change to the business model that Flipkart has done to adapt to the Indian market.

Flipkart is well-funded and probably will not need leverage to fund their growth.

On a forward looking basis on FY 2015 estimates, if you compared Flipkart with the top 3 listed retail players then Flipkart is trading at Enterprise Value / Sales of 1.6 times whereas the listed players Future Retail is trading at 0.7 times, Shoppers stop is trading at 0.74 times & Trent trades at 1.24 times.

Conclusion

On parameters of growth outlook, business model and balance sheet strength Flipkart scored hands down over the listed peers. Current profits and profitability is where it falters. However, if it does turn a corner in next 2 years. It might not look as expensive as it is looking right now.

Even though Flipkart valuations are apparently expensive, they might not be all that crazy. A look at international comparative will give a good perspective.

While the valuations of listed peers are surely on the lower side but probably justified until fundamentals change for the better.

Please read the following carefully and select your residency jurisdiction

*If you access this website by giving false declaration, you shall be solely liable/responsible for any adverse consequences suffered, legally as well as financially, pursuant to use of any information contained in this website.