IPL mania is again upon us, like every summer. The last few years, however, have seen a new feature added to these matches: the “Strategic Time Out”.

For those who are uninitiated, time outs in sports, often plays a strategic role that can end up altering the course of the game. Drawing up key plays, making substitutions, maintaining possessions and building strategies for the match ahead are the key features of a time out.

These matches and almost all sports, if you observe minutely, have many similarities to the markets. Markets are often run by emotions, full of paradoxes and cradled between the antonyms of supply-demand, greed-fear, recessions-growth, inflations-deflations.

Strategic Time Out – Inflexion Point

Back in June 2020, we argued that India was just entering a robust economic cycle, with plenty of room for growth. This sentiment was reaffirmed in January 2021 during our webinar with Shri Madhu Kela ji, where it became clear that we were not in bubble territory.

Last year, we hosted our own “VQ Inflexion Day,” where we extensively discussed the opportunities within mega trends that could potentially serve as significant wealth creators as the world embarks on the path of Energy Transition. India’s journey towards self-reliance (Atmanirbhar), coupled with its emergence as a preferred destination for the China +1 strategy, particularly in manufacturing and defence, presents yet another significant area for wealth

creation opportunities.

Excerpts from Inflexion Day

Which megatrends will define India’s future?

Ravi Dharamshi

Founder & CIO, ValueQuest

India a growth Oasis in a VUCA world

Sameer Shah

Co-founder ValueQuest

The patterns & framework of wealth creation

Varun Goenka

Fund Manager, ValueQuest

Strategic Time Out – Reflection Point

The prevailing concern in India today is about overvaluations and whether our markets are in a bubble. However, this view is an oversimplification of the situation.

As Warren Buffett rightly said:

In light of the significant events spanning from 2010 to 2020, such as the Rupee crisis, Demonetisation, GST implementation, NBFC crisis, and the unprecedented impact of the Covid pandemic, the trajectory of positive economic growth has been notably absent. Understandably, this prolonged period of uncertainty has left many discerning market observers cautious about the current upswing. While markets may have pre-empted a resurgence in economic activity, the underlying reality suggests that we are merely at the nascent stage of this recovery. Corporates, perhaps understandably so, remain apprehensive about committing to significant investments for the future until a more tangible and sustained economic rebound is evident.

Some of our own apprehensions about volatility materialised in the first quarter of 2024 itself. Significant volatility spurred by nudges from both regulators, RBI and SEBI has effectively reduced frothiness in the SME market and corrected valuations of mid and small caps as well. While this can be looked as the glass half empty, we look it as a glass half full as this intervention has probably set the stage for markets to emerge stronger as we move forward.

After the inflexion point, it’s a time of reflection and we find ourselves facing a similar dilemma, albeit at even higher market levels and

valuations.

Strategic Time Out – Observations and Navigation

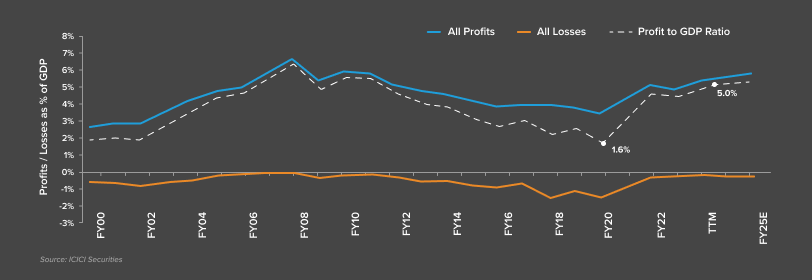

In December 2007, India’s GDP stood at $1.5 trillion, while its market capitalization peaked at $1.8 trillion. This marked the pinnacle, coinciding with India’s corporate profits after tax (PAT) reaching 7% of GDP, its highest point. Typically, markets reach their peak when there’s maximum growth and profits, leaving limited room for further profitability. Factors like leverage, compounded by external events, often trigger a downturn in the economic cycle, leading to prolonged and deeper value destruction.

However, the current conditions don’t reflect peak growth, profits, profitability, or leverage that typically precede such severe downturns. While a correction is always a possibility, it’s essential to heed Peter Lynch’s cautionary wisdom: “Far more money has been lost by investors in preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.” While it’s natural to anticipate downturns, excessive fixation on them can cause us to overlook potential opportunities. Despite inevitable market pullbacks, our investment strategy should remain focused on maintaining a prudent and balanced approach. We mustn’t let short-term fluctuations overshadow our long-term objectives.

From 2007 to 2020, India’s GDP surged from $1.5 trillion to $3 trillion, but corporate profits after tax (PAT) as a percentage of GDP plummeted from 7% to a mere 1% at the bottom of the Covid crisis. Since then, corporate PAT to GDP has rebounded to 4.8% currently. Initially, this uptick in corporate profits was fuelled by gross margin expansions and cost-cutting measures implemented during the pandemic. Much of the profits generated during this period were directed towards reducing debt burdens on balance sheets.

Since 2016, the Modi government has pursued various reforms aimed at long-term benefits but causing short-term disruptions, particularly in informal sectors of the economy. Initiatives such as the introduction of GST, demonetisation, the NBFC crisis, and the subsequent Covid-19 pandemic have acted as successive shocks to the informal economy, accelerating the process of formalisation.

In this current corporate profit expansion cycle, which began in March 2020, there’s a strong case to suggest that we may surpass the peak achieved in December 2007.

Here’s why:

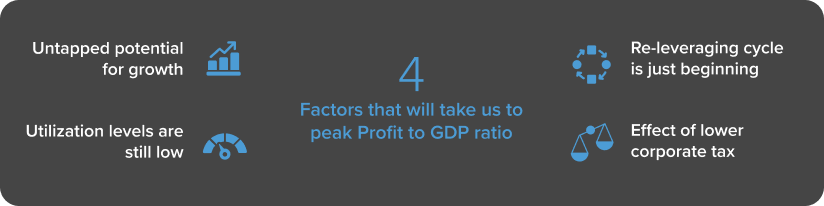

01– Not all engines of growth are firing yet: Unlike in 2007, when global growth was robust mainly due to China’s expansion, we are currently experiencing a more gradual recovery. This suggests that there’s still untapped potential for growth.

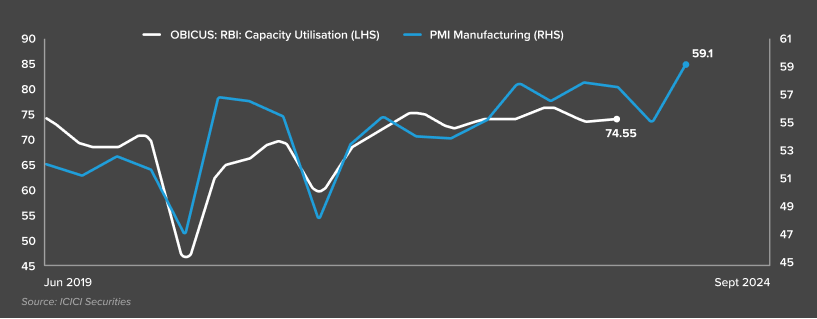

02– Utilization levels are below peak: Currently, we are operating at around 75% utilization, with the capex cycle expected to gain momentum as we approach 80% utilization. Increased utilization levels not only lead to higher profitability through operating leverage but also boost confidence in investing for the future.

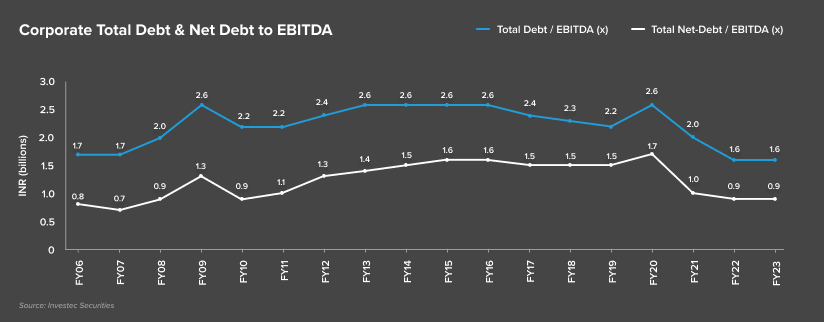

03– Re-leveraging cycle is just beginning: Indian corporate balance sheets remain relatively deleveraged, with Debt:Equity ratios at around 0.4x. As the economy rebounds, we can expect to see companies taking on more debt to fuel growth, contributing to increased profitability.

04– Lower corporate taxes: Compared to the previous cycle, corporate taxes are significantly lower, standing at 25% currently, with further incentives for greenfield capex at a reduced tax rate of 15%. This favourable tax environment is likely to result in higher accumulation of profits during this cycle compared to the previous one.

Taken together, these factors indicate the potential for a robust and sustained corporate profit expansion cycle, setting the stage for significant growth opportunities in the Indian economy.

The Indian economy is projected to reach $5 trillion by 2027, even if we consider a slight delay in achieving this target. Assuming we surpass the corporate tax to GDP ratio of the previous cycle, we could peak somewhere between 8% and 10%. For context, the US corporate profits after tax (PAT) to GDP peaked in 2021 at 14%.

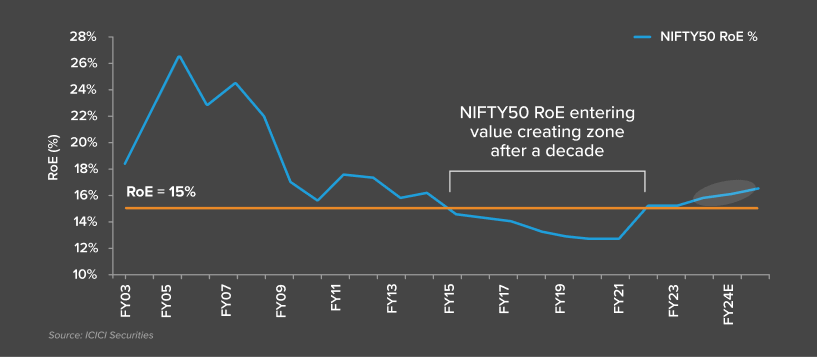

Even if we conservatively estimate a peak of 8% for this cycle, we could potentially see corporate profits ranging from $400 billion to $500 billion in the next 4 to 5 years. Return on equity (ROE) for Indian corporates hit a low of around 10% during the Covid bottom and has since expanded to 14%. However, with the expected expansion of corporate PAT to GDP over the next few years, we could ideally see ROE expanding to more than 20%

Such high growth coupled with high ROE is rare in today’s growth-starved world. This justifies the argument that India deserves a sustained higher multiple. Currently, the trailing PE of the entire market is at ~26x, and if we assume that there won’t be any further increase in multiples from here, then a corporate profit of $400 billion could lead to a market capitalisation of ~$10 trillion. This highlights the immense growth potential and attractiveness of the Indian market for investors.

However, the journey from point A to point B won’t be smooth sailing. As we discussed earlier, market volatility is not a flaw but a characteristic. It’s volatility that often presents us with favourable entry points. As Peter Bernstein says “Volatility is often a symptom of risk but is not a risk in and of itself. Volatility obscures the future but does not necessarily determine the future.”

Strategic Time Out – Game On

Markets are rich in valuation in a season of geopolitical news and shifts. Maintaining some dry powder will prove invaluable in seizing opportunities that may arise during market fluctuations. More importantly, it is imperative that we reduce our expectations on future returns and expand our time horizon to accommodate for market correction which is most likely in our current investment horizon.

In our base case scenario, a giant flywheel has been unleashed in India, one with several structural reforms and changes, be it supply related, being self-sufficient, in energy transition and financialisation or an impetus in manufacturing.

The wheel has just begun to roll and each turn of the flywheel builds upon work done earlier, compounding the investment of effort. A thousand times faster, then ten thousand times faster, then a hundred thousand times faster. This huge country is bound to fly forward with almost unstoppable momentum and thus continue remaining a bright spot in the investment horizon across the globe.

However, Indian markets may become further stretched, potentially reaching two standard deviations above their long-term average valuations. At such junctures, any reason could serve as a trigger for correction like current geopolitical tensions stemming from the Israel-Iran hostilities can introduce uncertainty into markets, prompting investors to reassess their risk exposure and strategies . It’s crucial to recognise that heightened valuations increase the market’s vulnerability to negative shocks.

Keeping both in mind, we continue to navigate the ups and downs of the market roller-coaster. We will make our best attempts at understanding the market cycles and how we can align ourselves to it and optimise our portfolio.

Until the next strategic time out – happy investing, and may your portfolios be as resilient as a cat with nine lives!

Warm regards,

Ravi Dharamshi

Founder and CIO, ValueQuest